Financial Risk Disclosure: Evidence From Albanian And Italian Companies

DOI:

https://doi.org/10.18502/kss.v1i2.656Abstract

In recent years standard setters, regulators and professional bodies worldwide have shown an increased interest in risk reporting. This has reflected the fallacy of the financial reporting model to communicate a company’s risk profile, the recent scandals and the financial crisis. The European Union, the International Accounting Standards Board (IASB) and other national standard settershave introduced specific requirements in order to impose companies to highlight the principal financial risks and uncertainties that they face.The idea is that high-quality risk disclosure help investors and other market participants in their decision-making process, by providing a better understanding of the risk exposures and risk management practices of companies.

Previous studies show large heterogeneity in risk reporting within individual countries and identify size as key determinant of risk disclosure. A few researches propose a cross-country investigation of risk reporting and to date there is a lack of evidence about companies operating in Southern Europe, especiallyin the Balkans.

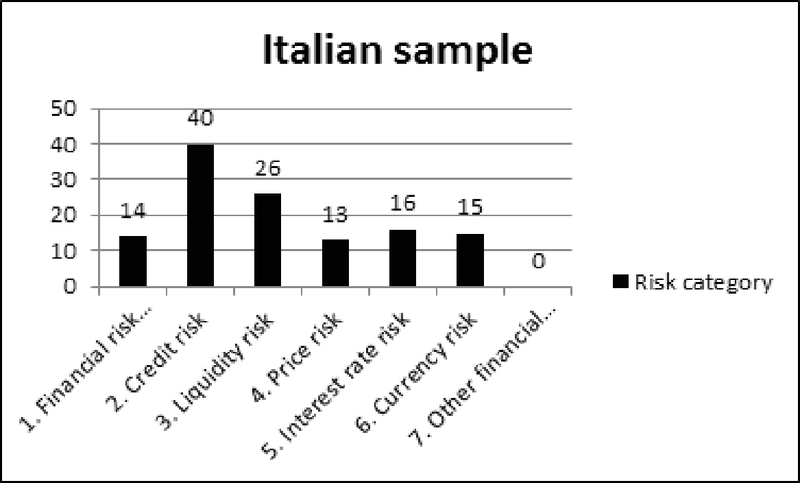

The aim of this study is twofold. First, we fill this gap by analyzingrisk reporting regulations in Albania and in Italy to examine the different requirements. Second, we examine risk information disclosed by a sample of 12 Albanian companies and 12 Italian companies within their annual reports, using content analysis. Due to small sample size we offer preliminary findings about financial risk disclosure. The results show that on average Albanian companies disclose less information on financial riskthan Italian companies. Different explanations can be given for this evidence: i) risk disclosure regulationis less incisive in Albania, because it is limited to inform investors about the relevance of financial instruments and the terms and conditions of loans; ii) Albanian companies have fewer incentives to disclose risk information than Italian companies.

Keywords: Financial risk disclosure, risk reporting, risk disclosure, content analysis, cross-country investigation

References

A. Adedeji and C. R. Baker, Financial reporting of derivatives before FRS 13. Derivatives Use, Trading and Regulation, 5, no. 1, 51–62, (1999).

A. Amran, A. Manaf Rosli Bin, and B. Che Haat Mohd Hassan, Risk reporting: An exploratory study on risk management disclosure in Malaysian annual reports, Managerial Auditing Journal, 24, no. 1, 39–57, (2009).

M. Bamber and K. McMeeking, An examination of voluntary financial instruments disclosures in excess of mandatory requirements by UK FTSE 100 non-financial firms, Journal of Applied Accounting Research, 11, no. 2, 133–153, (2010).

A. C. Beck, D. Campbell, and P. J. Shrives, Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British-German context, British Accounting Review, 42, no. 3, 207–222, (2010).

S. Beretta and S. Bozzolan, A framework for the analysis of firm risk communication, International Journal of Accounting, 39, no. 3, 265–288, (2004).

CFA. INSTITUTE, User perspectives on financial instrument risk disclosures under international financial reporting standards (IFRS).

W. Collins, E. S. Davie, and P. Weetmanf, Management Discussion and Analysis: An Evaluation of Practice in UK and US Companies, Accounting and Business Research, 23, no. 90, 123–137, (1993).

R. Deumes, Corporate risk reporting: A content analysis of narrative risk disclosures in prospectuses, Journal of Business Communication, 45, no. 2, 120–157, (2008).

M. Dobler, K. Lajili, and D. Zéghal, Attributes of corporate risk disclosure: An international investigation in the manufacturing sector, Journal of International Accounting Research, 10, no. 2, 1–22, (2011).

T. Dunne and C. Helliar, Financial reporting: FRS 13 derivatives disclosures. Accountancy, 131, no. 1318, 95–96, (2003).

T. Dunne, C. Helliar, D. Power, C. Mallin, K. Ow-Yong, and L. Moir, The introduction of derivatives reporting in the UK: a content analysis of FRS 13 disclosures, Journal of Derivatives Accounting, 1, no. 2, 205–219, (2004).

F. J. Elmy, L. P. Leguyader, T. Linsmeier, and J. , A review of initial filings under the SECs new market disclosure rules, The Journal of Corporate Accounting and Finance, 33–45, (1998).

K. Krippendorff, Content Analysis: An introduction to Its Methodology (2nded, Sage, Thousand Oaks, CA, 2004.

K. Lajili and D. Zéghal, A content analysis of risk management disclosures in canadian annual reports, Canadian Journal of Administrative Sciences, 22, no. 2, 125– 142, (2005).

P. M. Linsley and P. J. Shrives, Risk reporting: A study of risk disclosures in the annual reports of UK companies, British Accounting Review, 38, no. 4, 387–404, (2006).

P. M. Linsley and P. J. Shrives, Examining risk reporting in UK public companies, Journal of Risk Finance, 6, no. 4, 293–305, (2005).

T. J. Linsmeier, D. B. Thornton, M. Venkatachalam, and M. Welker, The effect of mandated market risk disclosures on trading volume sensitivity to interest rate, exchange rate, and commodity price movements, Accounting Review, 77, no. 2, 343– 377, (2002).

P. T. Lopes and L. L. Rodrigues, Accounting for financial instruments: An analysis of the determinants of disclosure in the Portuguese stock exchange, International Journal of Accounting, 42, no. 1, 25–56, (2007).

A. P. Marshall and P. Weetman, Information asymmetry in disclosure of foreign exchange risk management: Can regulation be effective? Journal of Economics and Business, 54, no. 1, 31–53, (2002).

A. Marshall and P. Weetman, Modelling transparency in disclosure: The case of foreign exchange risk management, Journal of Business Finance and Accounting, 34, no. 5-6, 705–739, (2007).

A. Marshall and P. Weetman, Managing interest rate risk and foreign exchange risk: disclosure objectives, policies and processes, ICAEW, Managing interest rate risk and foreign exchange risk: disclosure objectives, policies and processes, ICAEW, (2008).

A. Quagli, Comunicare il futuro. Franco Angeli, Comunicare il futuro. Franco Angeli, (2004).

D. T. Roulstone, Effect of SEC financial reporting release no. 48 on derivative and market risk disclosures, Accounting Horizons, 13, no. 4, 343–363, (1999).

R. Shkurti (Perri and J. Naqellari, Quality of financial and accounting information in Albania as perceived by the practicing accountants. The Journal of Accounting and Finance, Issue, 47, 110–123, (2010).

M. Woods and D. E. Marginson, Accounting for derivatives: An evaluation of reporting practice by UK Banks, European Accounting Review, 13, no. 2, 373–390, (2004).