Determinants Of The Trade Balance In The Turkish Economy

DOI:

https://doi.org/10.18502/kss.v1i2.654Abstract

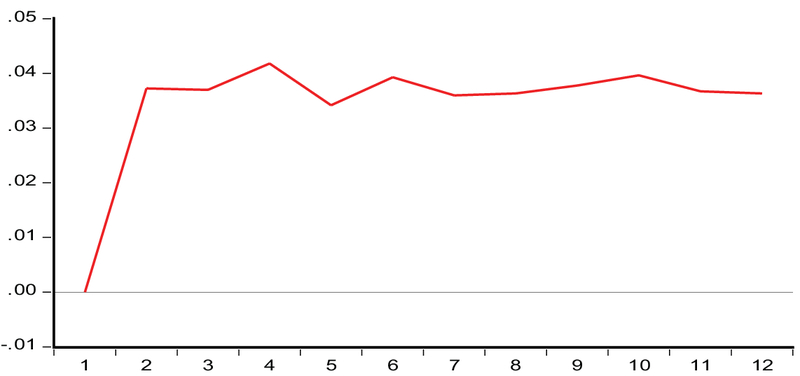

The Turkish economy has a long-run problem of trade deficits. Several efforts and different policies over the last 50 years could not find any permanent remedy to this problem which is an important source of external vulnerability for the Turkish economy. Thus, this study aims to shed light on the trade balance dynamics in Turkey via Johansen cointegration test, vector error correction model, and impulse-response analysis, for the period 1987–2015. Estimation results indicate that in the long-run an increase in real effective exchange rate improves trade balance, while an increase in Turkish (foreign) income improves (deteriorates) trade balance. In the short-run, real effective exchange rate has no impact on trade balance, while an increase in domestic and foreign income negatively affects the Turkish trade balance. The impulse-response analysis also shows that the J-curve hypothesis does not hold for the Turkish case.

Keywords: Trade Balance, Exchange Rate, J-curve, Turkey

References

S. r. Johansen, Likelihood-based inference in cointegrated vector autoregressive models, Oxford University Press, New York, 1995.

A. D. Krueger, Exchange Rate Determination, Cambridge University Press, Cambridge, UK, 1983.

E. Akbostanci, Dynamics of the trade balance: The Turkish J-curve, Emerging Markets Finance and Trade, 40, no. 5, 57–73, (2004).

M. Bahmani-Oskooee and T. J. Brooks, Bilateral J-Curve between US and Her Trading Partners, Weltwirtschaftliches Archiv, 135, no. 1, 156–165, (1999).

M. Bahmani-Oskooee and A. Ratha, The J-curve: A literature review, Applied Economics, 36, no. 13, 1377–1398, (2004).

J. C. Brada, A. M. Kutan, and S. Zhou, The exchange rate and the balance of trade: The Turkish experience, Journal of Development Studies, 33, no. 5, 675–692, (1997).

D. A. Dickey and W. A. Fuller, Distribution of the estimators for autoregressive time series with a unit root, Journal of the American Statistical Association, 74, no. 366, part 1, 427–431, (1979).

R. F. Engle and C. W. J. Granger, Co-integration and error correction: representation, estimation, and testing, Econometrica. Journal of the Econometric Society, 55, no. 2, 251–276, (1987).

F. Halicioglu, The J-curve dynamics of Turkey: An application of ARDL model, Applied Economics, 40, no. 18, 2423–2429, (2008).

S. r. Johansen, Statistical analysis of cointegration vectors, Journal of Economic Dynamics & Control, 12, no. 2-3, 231–254, (1988).

S. r. Johansen, Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models, Econometrica. Journal of the Econometric Society, 59, no. 6, 1551–1580, (1991).

S. Johansen and K. Juselius, Maximum Likelihood Estimation and Inference on Cointegration — With Applications to the Demand for Money, Oxford Bulletin of Economics and Statistics, 52, no. 2, 169–210, (1990).

H. B. Junz and R. R. Rhomberg, Price Competitiveness in Export Trade among Industrial Countries, American Economic Review, 63, no. 2, 412–418, (1973).

P. Kale, Turkeys Trade Balance in the Short and the Long Run: An Error Correction Modelling and Cointegration, 15, 27–56.

A. O. Krueger, Some Economic Costs of Exchange Control: The Turkish Case, Journal of Political Economy, 74, no. 5, 466–480, (1966).

S. P. Magee, Currency Contracts, Pass-Through, and Devaluation, Brookings Papers on Economic Activity, No. 1, 303–325, (1973).

P. C. B. Phillips and B. E. Hansen, Statistical inference in instrumental variables regression with

M. Rahman, M. Mustafa, and D. V. Burckel, Dynamics of the yen-dollar real exchange rate and the US-Japan real trade balance, Applied Economics, 29, no. 5, 661–664, (1997).

D. Rodrik, Premature Liberalization, Incomplete Stabilization: The Özal Decade in Turkey, Tech. Rep., Incomplete Stabilization, The Özal Decade in Turkey. NBER Working Paper, 1990.

A. K. Rose and J. L. Yellen, Is there a J-curve? Journal of Monetary Economics, 24, no. 1, 53–68, (1989).

T. Stucka, The Effects of Exchange Rate Change on the Trade Balance in Croatia, Tech. Rep., 2004.

M. B. Yusoff, The effects of real exchange rate on trade balance and domestic output: A case of Malaysia, International Trade Journal, 24, no. 2, 209–226, (2010).